Oil prices clawed their way back to the $50 per barrel level, up more than 85 percent from their February lows, but the market has fallen back about $48 due to a variety of concerns related to global economic weakness and the strength of the dollar. The oil price rally also stalled, in part, because the markets grew concerned about a restart of drilling from U.S. shale companies. The short-cycle nature of shale drilling could allow many operations to spring back to life rather quickly.

Oil prices clawed their way back to the $50 per barrel level, up more than 85 percent from their February lows, but the market has fallen back about $48 due to a variety of concerns related to global economic weakness and the strength of the dollar. The oil price rally also stalled, in part, because the markets grew concerned about a restart of drilling from U.S. shale companies. The short-cycle nature of shale drilling could allow many operations to spring back to life rather quickly.

Despite signs of life, expectations of a sudden surge of new oil production are unfounded. Across the industry, drilling restarts will be incremental rather than wholesale.

The recent increase in the U.S. rig count has given some credence to that belief, a sign that some companies are sending their crews back to work. The industry added 12 oil rigs in early June, the first time the rig count has increased over two consecutive weeks since August 2015.

Despite signs of life, expectations of a sudden surge of new oil production are unfounded. Across the industry, drilling restarts will be incremental rather than wholesale. New production could come online, but it will not be enough to offset the ongoing declines in the U.S. this year.

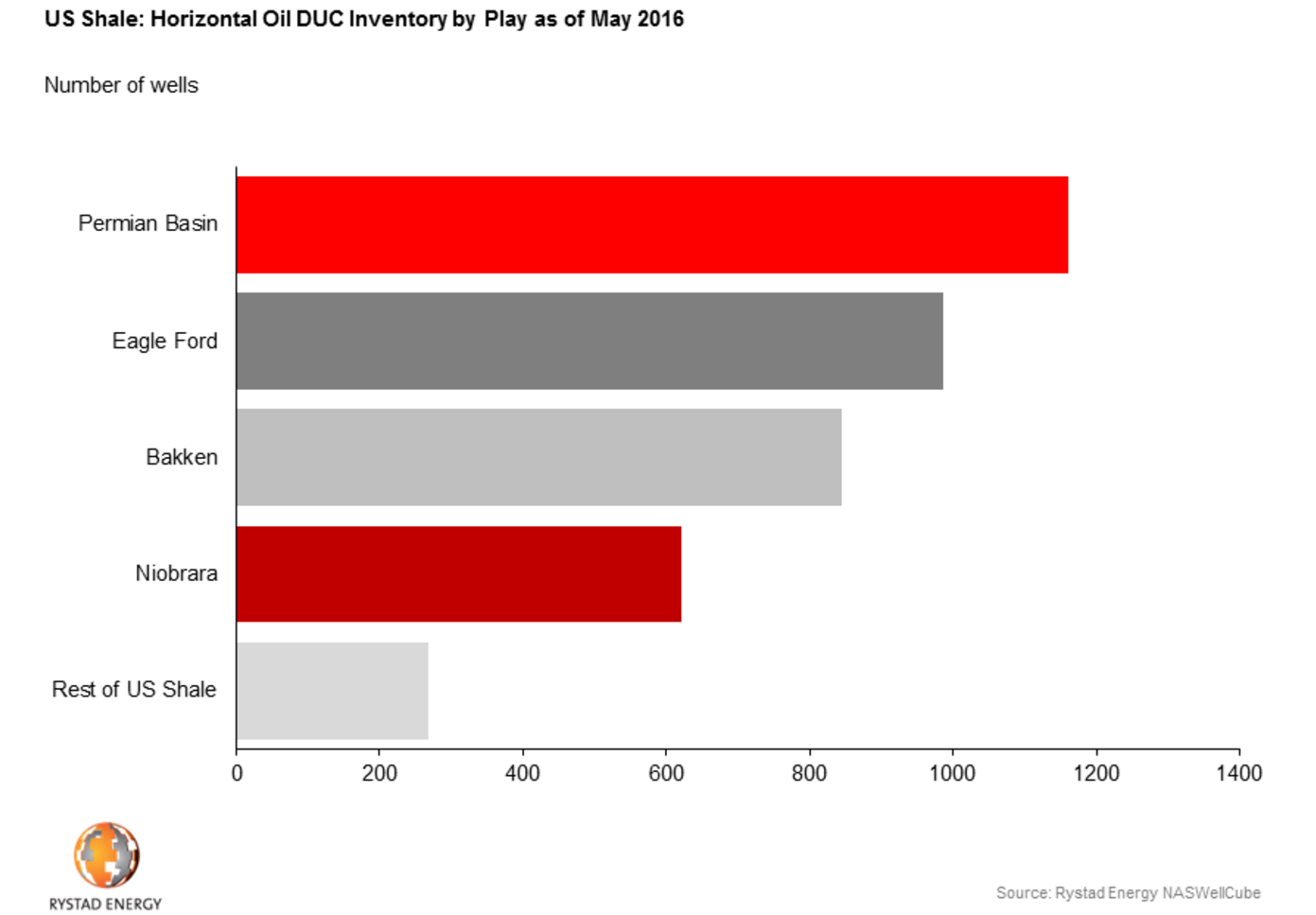

As oil prices rise, the first item on the industry’s agenda will be to work through the enormous backlog of drilled but uncompleted wells(DUCs). As oil prices crashed in 2014 and 2015, companies held off on completing wells in order to wait to sell their oil flows at a later date for a higher price. As time went on, the backlog of these DUCs—sometimes referred to as the “fracklog”—began to pile up. According to a Bloomberg Intelligence estimate, there were 4,290 DUCs at the end of 2015. A May 2016 estimate from Oslo-based Rystad Energy puts the figure at 3,900, over 90 percent of which are located in the four main shale plays of the Permian Basin, the Eagle Ford, the Bakken, and the Niobrara.

The CEO of Continental Resources, Harold Hamm, said on Bloomberg TV on June 9 that his company would begin completing some of the DUCs that it has sitting on the sidelines. Continental Resources is the largest producer in the Bakken Shale, where it is also in possession of the largest backlog of DUCs awaiting completion. The Oklahoma-based driller had 125 DUCs in the Bakken as of April 2016. The markets are watching Continental’s next moves for clues on what to expect from the region as a whole. North Dakota’s oil regulator, Lynn Helms, has said that $55 to $60 per barrel will be required before the fracklog is worked through. But Hamm’s comments were taken as a signal that some drilling is set to resume.

It is unclear if companies will rush to start completing DUCs en masse, but a few factors will motivate companies to move quickly. First, companies need cash. There have been at least 77 North American shale companies that have declared bankruptcy since the beginning of 2015 and many more with damaged balance sheets. Completing wells and bringing revenue streams online is an imperative as companies seek to shore up their financials.

Another motivation for companies to start working through the fracklog is to lock in the cost savings that resulted from the downturn. The oil industry has boasted of large cost reductions achieved over the past two years, savings achieved from tweaking drilling practices and streamlining operations. But only about 20 percent of those savings came from actual technological and operational improvements, according to Dan Guffey, vice president of equity research at Stifel Nicolaus, who spoke with Investors Business Daily in May. The rest could be transitory—they come from forcing desperate oilfield service companies and equipment suppliers to cut their prices. Those savings are cyclical and will quickly start to disappear as drilling picks up and suppliers raise their rates. Guffey believes the industry could rush to complete DUCs to take advantage of discounted oilfield services.

“This is the most hated bull market in history. Everyone thinks it will end.”

New drilling could add as much as 500,000 barrels per day to the market, according to Richard Westerdale, a director of policy analysis at the State Department’s Bureau of Energy Resources. To be sure, other estimates put the volumes at much more modest levels, but either way, there are large volumes of oil that could come online without much warning. “This is the most hated bull market in history,” Paul Sankey, an energy analyst at Wolfe Research LLC, said on Bloomberg Radio on June 10. “Everyone thinks it will end.”

New drilling needs higher prices

In a recently released report, Goldman Sachs struck a bearish view of oil prices, citing the potential for a weaker contraction from U.S. shale than expected. The investment bank said that “the industry’s focus on cost deflation and productivity gains raises the risk that near current prices, production continues to surprise to the upside.”

Oil speculators also hit the pause button, eyeing $50 oil and the prospect of new drilling. Short bets on crude prices from hedge funds posted the largest percentage gain in 11 months for the week ending on June 7, halting several weeks of players taking increasingly bullish positions.

The uptick in the rig count and the anecdotal announcements that companies are starting to work through the fracklog raises the prospect of new oil production coming online. However, a sudden rush of new production from the backlog of DUCs is likely a bit simplistic. Different companies will initiate completions of DUCs at different times, depending on their own cost structures and needs, which also vary from location to location. New production from DUCs will likely occur in fits and starts, rather than all at once.

Even if drillers want to move quickly, damage suffered to the industry workforce over the past two years could slow the pace of completions.

Even if drillers want to move quickly, damage suffered to the industry workforce over the past two years could slow the pace of completions. For example, Reuters reports that there were 45 fracking crews in the Bakken available for completion services in 2014. But because of the collapse of drilling activity, all but eight of them disappeared. It will take time to rebuild supply chains, preventing a sudden spike in production.

Moreover, there is a difference between completing wells that have already been drilled and drilling new wells. Although Continental’s Harold Hamm said his company would begin completing DUCs, he wouldn’t go as far as saying he would redeploy rigs to drill fresh wells. “We’d need to see WTI north of $60 before we ever thought about adding drilling rigs,” he told Bloomberg.

Even though the U.S. saw 12 rigs added in the first half of June, the rig count is still near record lows. The additions indicate that the market is bottoming out and could rebound from here, but the industry will need to deploy a lot more rigs in order to halt the production declines expected this year in the U.S. Wood Mackenzie estimates that U.S. oil production will likely stop declining only if another 50 to 100 rigs are added back into operation.

Goldman Sachs still sees U.S. oil production falling 430,000 barrels per day this year. Other forecasters agree. The EIA sees U.S. oil production averaging 8.6 million barrels per day in 2016 in its latestforecast, or about 100,000 barrels per day lower than what the U.S. produced in May, and down 1.1 mbd versus the peak hit in April 2015.

It is also not clear that oil prices will post more gains in the near term, which undermines the potential for a wave of U.S. supply to come on line. Goldman Sachs still sees an oversupplied market and record high levels of oil sitting in storage. The investment bank predicts that oil prices will stay below $50 per barrel for the next three months unless more unexpected supply disruptions occur. If crude prices remain flat or fall, companies deploying rigs for new drilling will remain the exception rather than the rule. “You start to have producers come back at $50, but a lot of them come in at $60,” Mark Watkins, a regional investment manager for The Private Client Group of U.S. Bank, told Bloomberg in an interview. The $60 price level is not necessarily right around the corner.

Even if WTI and Brent do rise further, there is no guarantee that all oil companies will respond with aggressive drilling plans. When oil prices rose last year to $60 per barrel, many companies thought the worst was over and jumped back into the fray only to see prices fall again. Still smarting from fleeting price rallies, U.S. shale companies will be much more cautious this time around. “[W]e understand the nature of this business and the price spikes. We’re not chasing those. We’re going to see stability before we even think about bringing rigs back in,” Continental Resources’ Harold Hamm said in May.

http://energyfuse.org/